A Definitive Approach to Life Insurance and Share Redemption in the Valuation of Family-Owned Businesses

In June 2024, the US Supreme Court, in a unanimous decision, ruled that proceeds from a corporate (or key person) life insurance should be added to the value of a business. Simple, right? So why is the decision in Connelly v. United States sending shockwaves through the valuation and estate planning exercises that go into an estate valuation? Let’s dive into the case and talk through its impact.

Facts:

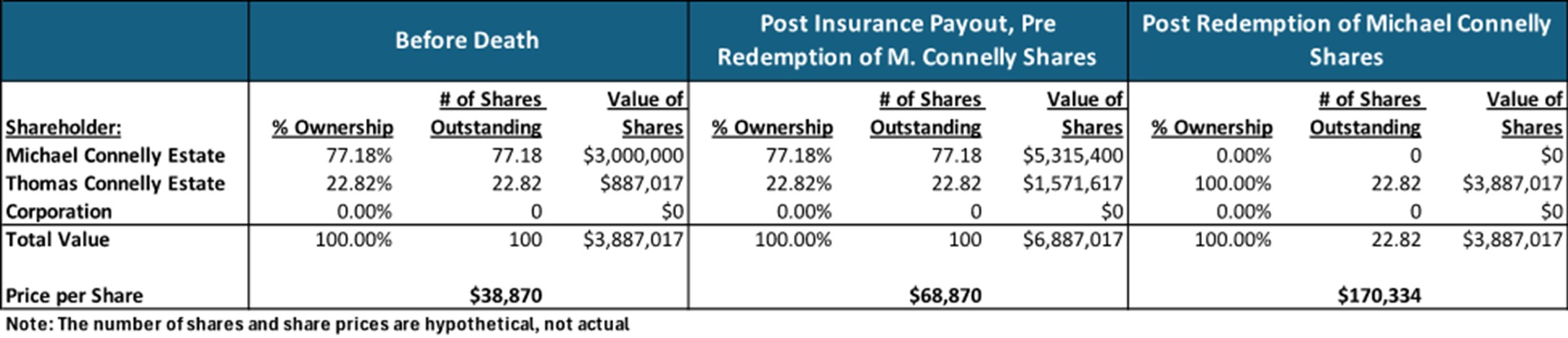

The case involved two brothers, Michael and Thomas Connelly, who were the sole shareholders of a corporation. They had a buy-sell agreement (BSA) in place, which was funded by life insurance policies held by the Corporation (as the beneficiary) on each other’s lives. The amount of insurance was $3.5 million for each brother. The buy-sell agreement was intended to ensure that upon the death of one brother, the surviving brother or the corporation could buy the deceased brother’s shares. The surviving brother had a right of first refusal with the Company required to buy the shares using the insurance proceeds if the surviving brother waived his right. When Michael passed away, Thomas did not buy the stock. The corporation was then required to buy the stock and used $3.5 million in life insurance proceeds to redeem Michael’s shares. An appraiser valued the business at $3.86 million and applied Michael’s ownership of 77.18% to this amount (or $2.98 million rounded up to $3.0 million). See calculations below.

ESTATE’S POSITION: 77.18% = $3.0 million

IRS Review:

The appraiser’s valuation of $3.8 million excluded the amount of the insurance proceeds used to buy out Michael’s estate and the Estate. However, the IRS took an opposing view, arguing that the overall value of the Company post-death was $6.86 million, $3 million in insurance proceeds used to redeem Michael’s 77.18% ownership plus $3.86 million of “other assets and other income generating potential”.[1] This substantial increase in the Company’s valuation and Michael’s interest ($6.86 million times 77.18% or $5.29 million), or an increase of $2.29 million. This increase raised the estate tax owed by $0.89 million, according to the Supreme Court’s calculation in the case syllabus.[2] See calculations below.

IRS’ POSITION: 77.18% = $5.3 million

Decision and Summary:

The Supreme Court ruled that the insurance proceeds were assets of the Company at the time of death and should be included in the estate. They argued that the obligation to buy the stock was not a liability; it was an equity obligation.[3]

References:

[1] Connelly v. United States, June 6, 2024. https://www.supremecourt.gov/opinions/23pdf/23-146_i42j.pdf

[2] Ibid.

[3] https://quickreadbuzz.com/2024/12/31/bv-kishel-caruso-valuation-lessons-from-connelly-v-united-states/

Valuation and Shareholder Analysis of Connelly

Impact:

The Connelly Decision clarified the valuation implications of using life insurance to fund buy-sell agreements. Additionally, it helped highlight the importance of ensuring that all key components of a buy-sell agreement are structured properly, especially in light of this ruling.

While we don’t draft BSAs, we provide feedback to our clients on the pros and cons of different pricing approaches and structures that are appropriate for each client’s circumstances and budget. Once armed with some ideas on how to structure these agreements, business owners should always consult with competent legal and tax counsel for additional feedback when drafting a buy-sell agreement. This process will help ensure that the contract is legally enforceable and that the business owner’s wishes are fulfilled.

Based on our read of hundreds of BSAs over the years, we have identified the following key characteristics of a properly planned and executed buy-sell agreement.

- Facilitates orderly transfer of interests upon certain events, affordably, at fair and reasonable values;

- Restricts who can own shares;

- Provides liquidity for a selling shareholder AND a viable funding plan for the Company;

- Increases visibility for planning: business, income tax, estate tax, retirement;

- Is negotiated early on while shareholders are aligned, healthy, and harmonious; and

- Is updated as conditions change

Specifically, as these BSAs relate to valuation, we note that most buy-sell agreements call for one, two, or three appraisers to determine value when a trigger event occurs. A multi-appraiser approach is more common with large companies and joint ventures. Small company BSA’s often suggest just one appraiser. Here are some thoughts on keeping us in mind for these valuations.

Exit Strategies Group:

As our clients prepare for this agreement, we recommend an initial benchmark valuation to quantify what is at stake and takes fear and mystery (and risk) out of the valuation process for the shareholders. Other than an initial valuation at the creation and execution of a BSA, we get involved in the following situations.

- Appraise Upon a Trigger Event: Exit Strategies routinely appraises shares when a BSA is triggered. We can be selected after a trigger event or named in the agreement.

- Periodic Valuations: Some buy-sell agreements call for annual or bi-annual valuations to maintain a current share price and help with buy-sell funding and planning. Exit Strategies provides initial valuations and updates.

- Price Formula Design: Some buy-sell agreements, particularly for very small businesses, use a price formula. There are pros and cons of using a price formula in a BSA. Clients that take a formula approach often engage Exit Strategies to design a formula that is more robust (better tracks future value) and replicable. As part of this process, we typically perform a benchmark valuation and meet with all shareholders to explain our valuation and formula, as well as incorporate their feedback.

- Buy-Sell Agreement Review: All buy-sell agreements, regardless of how well written, lose relevance over time and should be reviewed, tested, and updated periodically. We can review your BSA from business, economic, and valuation perspectives, identify potential problems, and recommend solutions. Sometimes, this includes testing a buy-sell price formula by performing the prescribed calculations or providing a business valuation for comparison. Performing an independent business valuation as part of a review can provide certainty and avoid surprises, time delays, and disputes later on.

Attorney and CPA CPE Offer:

Built off our firm’s many years of institutional experience and knowledge in helping clients structure and update BSAs, we utilize a proprietary database of the terms associated with BSAs to present the topic of “Avoiding Landmines in Buy-Sell Agreements: A Business Valuation Expert’s Perspective” to attorneys and CPAs for CPE credit. If you are interested in having us present this topic to your professional staff for CPE credit, please contact Joe Orlando at 503-925-5510 or jorlando@exitstrategiesgroup.com for more information.

Exit Strategies has certified appraisers who value control and minority ownership interests of private businesses for tax, financial reporting, and strategic purposes. If you’d like help in this regard or have any related questions, you can reach Pete Wilson at 510-590-7112 or pwilson@exitstrategiesgroup.com.

a

a