Acquistition Offers Can Vary Widely

Beauty is in the eye of the beholder; and when it comes to selling your business, value is in the eye of interested buyers.

As sell-side M&A advisors, we determine and agree on a probable selling price range with our clients, but we generally don’t set an asking price or discuss our clients’ value expectations with potential acquirers. Lower-middle-market businesses rarely go to market with an asking price.

Different buyers see different value in your business; so publishing an asking price is like setting a ceiling on what your business is worth.

Case in point …

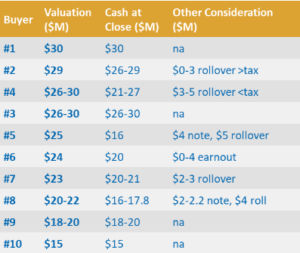

We recently represented a company that received 10 indications of interest (IOIs), from a combination of strategic and financial buyers, as shown in the following graphic. An IOI is an initial bid in which interested buyers submit an approximate price and general terms and conditions for completing a deal. At this stage in the process, buyers have signed an NDA and read a thorough prospectus on your company prepared by us, but they haven’t visited your company, met with you and your leadership team in person, or done any significant due diligence.

Notice the highest offer in this case was double the valuation of the lowest offer. This price range is fairly typical when we run a structured sale process.

These ten buyers saw exactly the same information; so why the dramatic range in value? In most cases, it comes down to motivation, synergies, perceived risk, and the buyer’s growth strategy.

At the end of the day, value is relative. When selling, you want acquirers to determine the value of your business to them. The buyer who will pay the most is usually the one who can leverage your business to the greatest extent. That said, predicting who is going to step up and make the strongest offers is way harder than it sounds.

In this case, after reviewing the ten IOIs with our client, we set up management meetings with four finalist buyers who offered the best combination of price, terms, and strategic and cultural fit. After management meetings, one of the finalists dropped out of the process because they felt they had better acquisition opportunities.

The other three finalists submitted final bids in the form of letters of intent (LOIs). An LOI is a more formal and detailed document and is usually exclusive. In the end, we sold the company for over $33 million.

To obtain the best price and terms available in the market, sellers need a structured sale process that brings all logical, qualified buyers to the table at the same time.

For further information on the M&A sale process or to discuss a potential business sale, merger or acquisition need, contact Exit Strategies Group’s founder and CEO Al Statz at 707-781-8580 or alstatz@exitstrategiesgroup.com.