A Difference of Opinions: Closely-Held vs. Venture-Backed Companies- Part 2 of 2

In Part 1 of 2 of this blog, I spoke about my transition from valuing venture-backed technology startups to valuing owner-operated small to middle-market businesses with $2 million to $50 million in revenue. As part of that discussion, I set the stage for three differences in how these types of businesses are valued, specifically differences in Diligence, Tools, and Approaches. Part 1 looked at Diligence and Tools, and Part 2 will complete this discussion with a focus on differences in business valuation Approaches and Discounts.

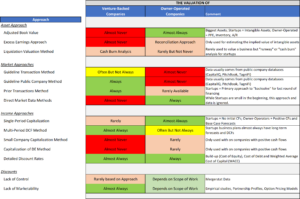

Valuation Approaches:

A valuation Approach is a general way of determining value using one or more business valuation methods. Below is a summary of each of the three fundamental approaches to determining value: Asset Approach, Market Approach, and Income Approach.

- The Asset Approach is based on the fair market value of a company’s underlying assets and liabilities. Generally speaking, the cost of duplicating or replacing each component is determined individually. Common asset-based methods are the a) Adjusted Book Value Method; b) Liquidation Value Method; and c) Replacement Cost Method.

- The Market Approach is based on the principle of substitution, meaning that for any investment an investor considers, there exist other investments with similar characteristics that are acceptable substitutes. “Prudent individuals will not pay more for something than they would pay for an equally desirable substitute.” The principle of substitution is applied by studying the values of comparable (or guideline) businesses to estimate a value for the company being appraised.

- The Income Approach considers the earnings capacity of a company. It values a business enterprise based on the present worth of its expected future benefit stream, adjusted for risk. The income approach operates on the theory that an investor will invest in businesses with similar investment characteristics, though not necessarily of the same business type.

Discounts

The values produced by the valuation methods used above may be subject to one or more adjustments referred to as discounts and premiums. The most common adjustments are control premiums, minority interest discounts (referred to as discounts for lack of control or “DLOC”), and discounts for lack of marketability (“DLOM”). Control refers to the extent to which an ownership interest controls the business entity. Marketability refers to liquidity, the extent to which an ownership interest can be sold quickly and turned into cash.

A controlling shareholder enjoys many benefits that are not enjoyed by minority interest owners. Minority interests are therefore usually worth less, often considerably less, than a proportionate share of the value of the total entity.[i] The types and magnitudes of the discounts/premiums applicable to an indicated value vary with the nature of the method, the data sources used to develop pricing multiples or rates of return, and the income normalization adjustments made. As noted above, our analysis using public company information assumes that any enterprise value is on a minority value because its capitalization is based on the value of a single share of minority equity.

Differences in Valuation Approaches and Methods and Discounts

An appraiser needs to consider all of these methods and potential discounts and decide which to use and which not to use. As outlined above, an appraiser’s approach and tools differ based on the scope of work and the type of company being valued.

This two-part blog offers a detailed review of how a business appraiser’s development of an opinion of value differs based on the ownership and size of the company being valued. I hope that this detail is both understandable and helpful.

Exit Strategies values control and minority ownership interests of private businesses for tax, financial reporting, and strategic purposes. If you’d like help in this regard or have any related questions, you can reach Joe Orlando, ASA at 503-925-5510 or jorlando@exitstrategiesgroup.com.

[i] Jay E. Fishman, Shannon P. Pratt, J. Clifford Griffith, and James R. Hitchner. PPC’s Guide to Business Valuations, Twentieth Edition, (Fort Worth, TX: Thomson Reuters, 2010), Volume 2, p. 803.5.